Arta Bārdule  ,

Edgars Jūrmalis,

Zane Lībiete,

Ilze Pauliņa,

Jānis Donis,

Agita Treimane

,

Edgars Jūrmalis,

Zane Lībiete,

Ilze Pauliņa,

Jānis Donis,

Agita Treimane

Use of retail market data to assess prices and flows of non-wood forest products in Latvia

Bārdule A., Jūrmalis E., Lībiete Z., Pauliņa I., Donis J., Treimane A. (2020). Use of retail market data to assess prices and flows of non-wood forest products in Latvia. Silva Fennica vol. 54 no. 3 article id 10341. https://doi.org/10.14214/sf.10341

Highlights

- Retail prices of non-wood forest products (NWFPs) may be used to study lifestyle-related consumption patterns

- While retail sales of NWFPs may increase household budgets, this source of income is highly variable due to varying meteorological conditions

- NWFP retail price analysis illustrates aspect of household economies not recorded in official statistics and cash flows of declared income.

Abstract

In northern Europe, largest part of non-wood forest products (NWFPs) are gathered for recreational purposes and household consumption, but considerable amount of forest berries and mushrooms are sold as well. Retail market, largely invisible for the official statistics, reveals the lifestyle-related aspects of NWFP trade and may help to understand the flows of this ecosystem service when information on wholesale trade is inaccessible. The prices and flows of most common NWFPs – edible berries, mushrooms and tree sap – in the retail market in Latvia in 2017 and 2018 were analysed based on direct interviews with the sellers in marketplaces and telephone interviews with online retailers. The mean retail prices of NWFPs were compared between statistical regions and years and correlated with socio-economic data and forest characteristics. The directions of the NWFP flows were analysed according to the place of origin and place of retail sales. The highest prices were recorded for stinkhorn (Phallus impudicus Pers.) and Boletes spp. among mushrooms, for wild strawberries (Fragaria vesca L.) among berries and for maple (Acer platanoides L.) sap in the product group of tree sap. The retail price of the same products differed between years, most likely due to the product availability, largely caused by meteorological conditions. In more than half of the cases of recorded sales, NWFPs were consumed in the same region as they were gathered. For other cases of sales, the capital, Rīga, was the main service benefitting area of NWFP retail trade, and the largest part of the products originated from the two closest statistical regions.

Keywords

forest berries;

mushrooms;

provisional ecosystem services;

retail prices;

spatial flows of NWFPs;

tree sap

-

Bārdule,

Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169

E-mail

arta.bardule@silava.lv

- Jūrmalis, Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169 E-mail edgars.jurmalis@silava.lv

- Lībiete, Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169 E-mail zane.libiete@silava.lv

- Pauliņa, Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169 E-mail paulina.ilze@gmail.com

- Donis, Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169 E-mail janis.donis@silava.lv

- Treimane, Latvian State Forest Research Institute “Silava”, Rigas str. 111, Salaspils, Latvia, LV-2169; University of Latvia, Jelgavas str. 1, Riga, Latvia, LV-1004 E-mail agita.treimane@silava.lv

Received 23 March 2020 Accepted 9 June 2020 Published 25 June 2020

Views 84993

Available at https://doi.org/10.14214/sf.10341 | Download PDF

1 Introduction

With the growing importance of the bioeconomy, non-wood forest products, “products of biological origin other than wood derived from forests, other wooded land and trees outside forests” (FAO 2015), are becoming increasingly significant, along with timber and energy wood, in both the global and the regional context. While the largest share of the NWFPs is still used locally for household purposes (FAO 2010) and forests are found to provide important dietary supplements for households and communities close to tropical forests (Rowland et al. 2016), a comprehensive literature review has demonstrated that the extraction and sales of NWFPs represent an important additional income to household budgets, especially in less developed countries (Stanley et al. 2012).

The interest in wild forest products in Europe has shown an increasing trend as well, demonstrating the shift of the society’s focus towards more vital natural ecological processes and rewilding as well as renewed interest in the cultural services provided by forests, expressed as heritage values and recreational experiences (Wiersum 2017). As a major ecosystem service, the provision of NWFPs is considered vital for understanding and attaining the multifunctionality of forest areas, although trade-offs exist between some management regimes and some forestry actions (Lõhmus and Remm 2017; Kurttila et al. 2018). Recreation and the collection of NWFPs could, in turn, be considered synergetic, depending on the economic importance of the selected NWFPs in different regions (Stryamets et al. 2015; Wiersum 2017). For example, the research conducted by Kangas and Niemeläinen (1996) in Finland has shown that the beauty of the landscape, biodiversity, berries and mushrooms are thought to be important main values of forests. In a study carried out in 2014, it was calculated that at least 65 million members of the EU population gather wild products for consumption but at least 100 million consume such products (Schulp et al. 2014), indicating the cultural and socioeconomic importance of NWFPs. Foraging for wild berries and mushrooms as a culturally embedded practice and important recreational activity is recorded in publications by numerous Nordic, Baltic, Central and Western European authors (Pouta et al. 2006; Martinez de Aragon et al. 2011; Sisak et al. 2016; Grivins and Tisenkopfs 2018).

In Northern Europe especially, the extraction and use of NWFPs have ancient and persistent traditions, despite the fact that urbanisation processes have put a distance between the human population and the forest ecosystems (Saastamoinen et al. 2014). One of the most important factors influencing the use and amount of NWFPs is the access to these resources. In the Nordic countries, the so-called “everyman’s right” is in force, entitling every person to move freely in nature irrespective of ownership. These rights also apply to the use of NWFPs, except protected plant species, products growing in trees (e.g., Inonotus obliquus (Pers.: Fr.) Pilat fungi used for medicinal purposes) and specifically marked areas, designed, for example, for nature protection (Jeanrenaud 2008; Parviainen 2015). In Latvia, similar regulations are in force. People are allowed free movement in all state, municipality and private forests, unless there are prohibition signs, and it is permitted to gather NWFPs for private consumption outside protected nature areas (Latvijas Republikas Saeima 2000).

Economic considerations are often as important as changes in the perception of nature and lifestyle. In several regions of Europe, the importance of NWFPs is increasing in the context of promoting the bioeconomy in rural areas (Calama et al. 2010; Tahvanainen et al. 2016). In Nordic and Baltic countries, forest berries and mushrooms are gathered in economically significant amounts, both as a market good and for private consumption (Cesaro et al. 1995). During the recent decades the gathering of wild products in several European countries has transformed from primarily recreational activity and culturally-rooted practice into commercial activity (Keča et al. 2013; Sisek et al. 2016; Hamunen et al. 2019). According to a study carried out in 2011, 77% of the inhabitants of Latvia had gathered NWFPs in 2010 (Donis and Straupe 2011). The main NWFPs were berries (bilberries (Vaccinium myrtillus L.), lingonberries (Vaccinium vitis-idaea L.) and cranberries (Oxycoccus palustris Pers.)), mushrooms and birch (Betula spp.) sap. While berry and mushroom picking during the summer in Latvia is considered an important recreational activity by 53.5% of the population (Donis 2018), this forest ecosystem service has an important economic dimension as well. According to the pilot study carried out by the Latvian State Forest Research Institute “Silava” in 2016, wild plants and their products (according to the Common International Classification of Ecosystem Services (2013)) were evaluated as the most important provisioning forest ecosystem service (Lībiete 2017).

The income from the sales of NWFPs worldwide provides substantial economic support for many households in rural areas and serve as important means for poverty alleviation (Neumann and Hirsch 2000; Shackleton and Gumbo 2010; Keča et al. 2013; Grivins et al. 2016). High socio-economic importance of non-timber forest products has been recorded, for example, by Kovalčík (2014) in Slovakia, Sisak et al. (2016) in Czech Republic and Keča et al. (2013) in Serbia. In a regional context, NWFPs are also considered important aspects of international trade and export subjects, as demonstrated by healthy lifestyle trends and the increasing popularity of natural, rural products. This, in turn, involves more stakeholders and business owners and increases the complexity of NWFP flows from forest sites to final consumers (Hamunen et al. 2019). Study performed by Weiss et al. (2020) demonstrates new dimensions of business opportunities related to non-wood forest products in Europe and North America, centred on both consumption practices and cultural aspects, for example, promotion of wild products in close conjunction with recreation in nature areas. At the same time, more intense foraging for non-wood forest products and unsustainable gathering practices may raise concerns for biodiversity, as noted by, for example, Martinez de Aragon et al. (2011) and Sisak et al. (2016). Consequently, there is a recurring debate about trade-offs in the use of different forest ecosystem services, as well as implementation of various policy instruments to regulate the gathering of NWFPs, like permits, charges and legal measures. However, as concluded by Stryamets et al. (2020), governance of forest resources is complicated due to the complexity of their importance for economy, nature conservation, societal and cultural aspects and the existing legal frameworks are often complex, overlapping and lacking clarity.

Berry and mushroom picking gained much larger economic importance after the economic crisis of 2009 with the rise of unemployment, especially in rural areas (Grīviņš 2015; Grivins and Tisenkopfs 2018). The bulk purchase of NWFPs from the inhabitants and consequent wholesale to processing enterprises are still a popular form of seasonal entrepreneurship, and berry and mushroom purchase points during the summer and autumn are active throughout the territory of Latvia. Grivins (2016) and Grivins and Tisenkopfs (2018), who studied the wild bilberry trade, estimated that there could be between 500 and 800 purchase points in the country. With time, the dealers of forest products have become more integrated into the global markets, and, while the sector remains to a large extent unregulated by the state and the presence of “grey” entrepreneurship practices is strong, forest berry picking has an important social dimension in strengthening social relations and empowering rural communities (Grivins 2016; Grivins et al. 2016).

Apart from wholesale and large-scale trade, the local trade in wild forest products has a stable position in the retail market. In the Nordic and Baltic countries, forest berries and mushrooms are important ingredients for the national cuisine; moreover, during the last decade, the consumption of high quality, healthy and ecologically clean local products has gained substantial popularity. Not all inhabitants have the time and possibilities to gather NWFPs themselves; therefore, these are often purchased in markets where there is a wide offer of local products, both cultivated vegetables and fruits from farms and wild berries and mushrooms from forests. The demand for these products is especially high in the urban environment reflecting lifestyle-driven aspects of NWFP consumption. At the same time, for example, in Latvia, retail market of NWFPs remains largely outside the scope of any official statistics, while the income tax needs to be paid only if the income from sales exceeds 3000 EUR within one calendar year (The Supreme Council of the Republic of Latvia 1993). Thus, small-scale sales that do not reach this threshold remain unrecorded.

Multifunctional forestry should take into consideration various ecosystem services provided by forests. The need to plan for diversity involves the need for information considering the use patterns of the ecosystem services of interest. Especially in the case of forest product analysis, biophysical data obtained within the forest need to be complemented with information about the further movement of these products to understand better the supply–demand relationships. Due to high share of “grey” entrepreneurship, forest products’ wholesale trade is largely inaccessible for analysis, however, an assumption can be safely made that a considerable part of these products is exported. Therefore, to obtain information about domestic NWFP market, we chose to study the retail market of non-wood forest products in Latvia from two aspects: firstly, the retail price differences of NWFPs and, secondly, the directions of the NWFP flows in Latvia. This paper aims to highlight the possibilities to use retail market monitoring data in the analysis of NWFPs within the ecosystem service framework, as well as to reveal short-term trends in prices and flows of these products in Latvia. For this purpose results of two consecutive monitoring years – 2017 and 2018 – were used.

2 Material and methods

Information about the prices and flow directions of NWFPs were obtained with two methods: 1) direct interviews with sellers in the marketplaces in Rīga; 2) telephone interviews using online information (advertising servers and social networks). Direct interviews were carried out in all the largest markets of Rīga: Āgenskalna market (Zemgales suburb), Čiekurkalna market (Ziemeļu suburb), Purvciema market (Vidzemes suburb), Ķengaraga market (Latgales suburb), Central market and Vidzemes market in the Centra district. These markets are the most popular among the sellers from Rīga vicinity and other regions of Latvia and are the best known and most often visited by consumers. Direct interviews were conducted in March and April 2017 and 2018 (for information on maple and birch sap) and from the beginning of July to the beginning of October of the respective years (for information on forest berries and mushrooms), with a frequency of every two weeks. Telephone interviews were conducted according to the information found on advertising servers (ss.com) and social networks (Facebook) several times during the season, from April to October 2017 and 2018.

Information on the following NWFPs was analysed: 1) forest berries (bilberries (V. myrtillus), lingonberries (V. vitis-idaea), wild strawberries (Fragaria vesca L.), wild raspberries (Rubus idaeus L.), cloudberries (Rubus chamaemorus L.) and cranberries (O. palustris)); 2) forest mushrooms (chanterelles (Cantharellus cibarius Fries), boletes (Boletus edulis Bull.:Fr. and other kindred species and other Boletaceae mushrooms) and stinkhorn (Phallus impudicus Pers.)); and 3) birch (Betula spp.) and maple (Acer platanoides L.) sap. The following information was recorded for each case of sales: the species, place of gathering, place of sale, price for 1 L or 1 kg (depending on each individual case), type of the interview (direct or phone interview) and remarks.

In total, information about 267 berry sales (90 from direct and 177 from telephone interviews), 193 mushroom sales (106 from direct and 87 from telephone interviews) and 100 tree sap sales (36 from direct and 64 from telephone interviews) was collected during the season of 2017. Information about 424 berry sales (221 from direct and 203 from telephone interviews), 154 mushroom sales (117 from direct and 37 from telephone interviews) and 94 tree sap sales (26 from direct and 68 from telephone interviews) was collected during the season of 2018.

All the data analysis was conducted in R. Only comparable cases were included in each run of the statistical analyses (data sets of the same NWFPs but different units of amount – weight or volume – were analysed separately). Individual records were merged into statistical regions (NUTS 3, Fig. 1): Rīga, Pierīga, Zemgale, Vidzeme, Latgale and Kurzeme (Cabinet Order No 271 2004) according to the place of sales. The mean retail prices of the NWFPs were compared between the statistical regions where they were sold. Statistical differences between classes (at the significance level α = 0.05) were analysed with the Wilcoxon rank sum test with continuity correction.

Fig. 1. Statistical regions of Latvia.

The mean retail prices of NWFPs were analysed in relation to socioeconomic indices of the population and forest characteristics within the NUTS 3 statistical regions. The respective indices are shown in Table 1 and Table 2, respectively. The relationship strength was determined with Pearson’s correlation analysis and relationship significance with linear regression analysis (response variables were retail prices of NWFPs, explanatory variables were socioeconomic indices of the population and forest characteristics within the NUTS 3 statistical regions, significance level α was 0.05).

| Table 1. Characterization of population (age 15–74) in different statistical regions of Latvia in 2017 and 2018 (Central Statistical Bureau of Latvia 2019). | ||||||||

| Parameter, unit | Year | Statistical regions of Latvia | ||||||

| Rīga | Pierīga | Kurzeme | Zemgale | Latgale | Vidzeme | |||

| Population, number (thousand) | 2017 | 468.2 | 267.2 | 178.2 | 171.4 | 199.3 | 139.0 | |

| 2018 | 465.7 | 268.5 | 175.8 | 169.2 | 195.3 | 136.3 | ||

| Economically active population*, number (thousand) | total | 2017 | 336.9 | 188.4 | 118.4 | 114.9 | 127.2 | 94.5 |

| 2018 | 341.6 | 191.3 | 117.5 | 112.6 | 124.8 | 94.4 | ||

| employed | 2017 | 310.8 | 177.3 | 107.9 | 104.2 | 109.3 | 85.3 | |

| 2018 | 319.3 | 182.4 | 108.3 | 103.5 | 110.0 | 85.9 | ||

| unemployed | 2017 | 26.1 | 11.1 | 10.4 | 10.7 | 17.9 | 9.2 | |

| 2018 | 22.3 | 8.9 | 9.1 | 9.1 | 14.7 | 8.5 | ||

| Economically inactive population**, number (thousand) | 2017 | 131.3 | 78.8 | 59.8 | 56.5 | 72.1 | 44.5 | |

| 2018 | 124.1 | 77.2 | 58.3 | 56.6 | 70.5 | 41.9 | ||

| Unemployment rate, % | 2017 | 7.8 | 5.9 | 8.8 | 9.3 | 14.0 | 9.7 | |

| 2018 | 6.5 | 4.7 | 7.8 | 8.1 | 11.8 | 9.0 | ||

| Number of people with higher education, number (thousand) | 2017 | 184.7 | 83.5 | 35.2 | 38.1 | 44.1 | 26.3 | |

| 2018 | 179.8 | 83.0 | 37.5 | 37.9 | 43.8 | 29.7 | ||

| Average monthly salaries (Gross/Net), euro | 2017 | 1044/758 | 871/640 | 775/568 | 786/579 | 640/471 | 739/544 | |

| 2018 | 1129/829 | 949/705 | 858/641 | 848/634 | 701/529 | 803/604 | ||

| * Economically active population – active population consists of employed persons and unemployed persons actively seeking a job. ** Economically inactive population – persons who can neither be classified as employed nor as unemployed persons (pupils, students, non–working pensioners, etc.). | ||||||||

| Table 2. Characterization of forest in different statistical regions of Latvia (Latvian NFI data, 2015). | ||||||

| Parameter, unit | Statistical regions of Latvia | |||||

| Rīga | Pierīga | Kurzeme | Zemgale | Latgale | Vidzeme | |

| Forest area, kha | 5.27 | 550.30 | 770.91 | 428.80 | 595.99 | 889.82 |

| Forest cover, % of total land area | 17.3 | 54.3 | 56.7 | 39.9 | 41.0 | 58.3 |

| Estimated potential mean bilberry yield*, kg ha–1 | 27.6 | 13.1 | 19.3 | 10.0 | 6.8 | 8.6 |

| Estimated total bilberry yield in the statistical region**, kt | 0.15 | 7.22 | 14.90 | 4.29 | 4.05 | 7.64 |

| Estimated potential mean lingonberry yield*, kg ha–1 | 12.3 | 4.2 | 5.5 | 3.3 | 2.4 | 2.7 |

| Estimated total lingonberry yield in the statistical region**, kt | 0.06 | 2.29 | 4.23 | 1.40 | 1.45 | 2.42 |

| * Potential mean berry yields are calculated according to equations that take into consideration site type, stand age and stand density. Information on projective cover of specific berry species is obtained from the NFI data. ** Information on the cover of different forest types and their properties in the statistical region is obtained from State Forest Register. | ||||||

Ecosystem service flows were analysed in more detail according to the concepts provided by Burkhard et al. (2014). The places of gathering were labelled as ecosystem service providing units (SPUs) and the places of sale as ecosystem service benefitting areas (SBAs). The data for the analysis were divided into two sets and smaller sub-sets as described further. Data from the telephone interviews were used to identify the main directions of the flows of ecosystem services for berries (all species combined), mushrooms (all species combined) and birch sap. Data from the direct interviews were used to determine the main SPU in relation to the main SBA – Rīga. In both cases, the analysis was initially carried out on the level of statistical regions, and then, in cases in which sufficiently detailed information was available, the county was used as the smallest unit for the analysis.

3 Results

3.1 Prices of different NWFPs in the statistical regions

The total recorded number of tree sap sales was similar in 2017 and 2018. For mushrooms, the number of recorded sales was greater in 2017, but for forest berries, the opposite was true. In all the product categories, most of the NWFPs in the market originated from Pierīga statistical region, but the smallest amount was obtained in Rīga statistical region (Table 3). This remained true also if the direct interviews conducted in the marketplaces in Rīga were excluded, but the differences between statistical regions decreased somewhat in this case.

| Table 3. Non-wood forest product sales according to the place of origin in 2017 and 2018 in Latvia. | ||||||||||||

| Statistical regions of Latvia | Birch and maple sap | Mushrooms | Berries | |||||||||

| count | share of total count, % | count | share of total count, % | count | share of total count, % | |||||||

| 2017 | 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | 2018 | 2017 | 2018 | |

| Kurzeme | 14 | 5 | 14 | 5 | 47 | 20 | 24 | 13 | 23 | 47 | 9 | 11 |

| Latgale | 3 | 2 | 3 | 2 | 9 | 10 | 4 | 6 | 21 | 53 | 8 | 13 |

| Vidzeme | 8 | 11 | 8 | 12 | 19 | 16 | 10 | 10 | 58 | 45 | 22 | 11 |

| Zemgale | 26 | 17 | 26 | 18 | 25 | 24 | 13 | 16 | 47 | 72 | 18 | 17 |

| Pierīga | 47 | 54 | 47 | 57 | 87 | 76 | 45 | 49 | 103 | 173 | 38 | 41 |

| Rīga | 0 | 0 | 0 | 0 | 3 | 1 | 2 | 1 | 9 | 1 | 3 | <1 |

| Unknown | 2 | 5 | 2 | 5 | 3 | 7 | 2 | 5 | 6 | 33 | 2 | 8 |

| Total | 100 | 94 | 100 | 100 | 193 | 154 | 100 | 100 | 267 | 424 | 100 | 100 |

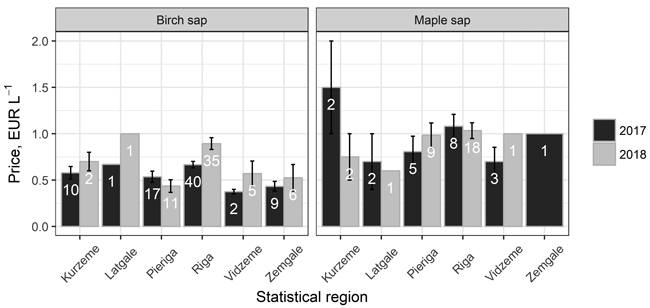

Fig. 2 shows the mean birch and maple sap prices in the retail market in the statistical regions of Latvia in 2017 and 2018. In 2017, the mean price of birch sap in different statistical regions of Latvia varied from 0.38 EUR L–1 (place of sale – Vidzeme statistical region) to 0.67 EUR L–1 (place of sale – Rīga statistical region). The average price of birch sap was significantly higher (p = 0.004) in 2018 (0.74 EUR L–1) than in 2017 (0.59 EUR L–1). The mean price of birch sap in 2018 varied from 0.45 EUR L–1 (place of sale – Pierīga statistical region) to 0.88 EUR L–1 (place of sale – Rīga statistical region), excluding Latgale statistical region, where only one trade case was registered (price 1.00 EUR L–1). In 2017, the mean price of birch sap was significantly higher in the marketplaces of Rīga than in all the other statistical regions (p = 0.004), excluding Latgale statistical region, where only one case of a sale was registered. In 2018, the mean price of birch sap was significantly higher in the marketplaces of Rīga than in Pierīga statistical region (p < 0.001).

Fig. 2. Mean retail price of birch and maple sap in the 2017 and 2018 season by statistical region. White figures in the bars indicate number of cases included in the calculation of mean price.

In 2017, the highest average price for maple sap was recorded in Kurzeme statistical region (mean price 1.50 EUR L–1), but, as the number of sales there was very small (n = 2), no statistically significant differences were detected between Kurzeme and other statistical regions. The lowest price for maple sap in 2017 was registered in Latgale and Vidzeme statistical regions (mean price 0.70 EUR L–1). The average price of maple sap was a little higher in 2018 (0.99 EUR L–1) than in 2017 (0.96 EUR L–1), but there was no statistically significant difference between the average price of maple sap in 2017 and that in 2018 (p = 0.816). In 2018, the highest average price for maple sap was registered in Rīga statistical region (mean price 1.03 EUR L–1), but the lowest price for maple sap in 2018 was registered in Latgale statistical region (mean price 0.60 EUR L–1).

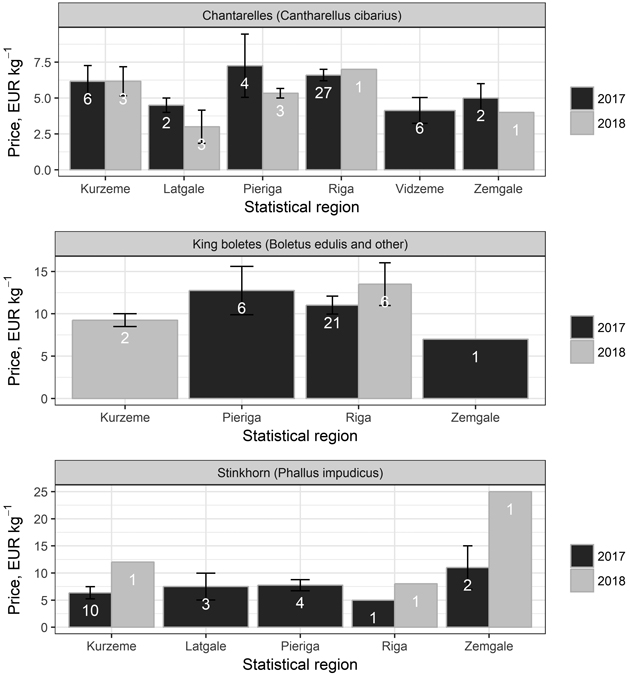

Fig. 3 summarizes the information on the mean retail price of chanterelles, king boletes and stinkhorn in 2017 and 2018. The mean retail price for 1 kg of chanterelles in different statistical regions of Latvia varied from 4.13 EUR kg–1 (in Vidzeme statistical region) to 7.25 EUR kg–1 (in Pierīga statistical region) in 2017 and from 3.00 EUR kg–1 (in Latgale statistical region) to 7.00 EUR kg–1 (in Rīga statistical region) in 2018; furthermore, there is no statistically significant difference between the mean retail price for 1 kg of mushrooms in 2017 and that in 2018 (p = 0.157). No significant differences between the mean price for 1 kg of chanterelles in Rīga, Pierīga and Kurzeme statistical regions were detected (p > 0.05 and the mean price was 6.60 EUR kg–1 in 2017 and 5.93 EUR kg–1 in 2018). The mean retail price of chanterelles in the above-mentioned regions was significantly higher than that in Latgale, Vidzeme and Zemgale statistical regions (p = 0.009 and the mean price was 4.38 EUR kg–1 in 2017, but p = 0.014 and the mean price was 3.25 EUR kg–1 in 2018).

Fig. 3. Mean retail price of forest mushrooms in the 2017 and 2018 season by statistical region. White figures in the bars indicate number of cases included in the calculation of mean price.

In 2017, sales of king boletes and other kindred mushroom species were recorded only in Rīga, Pierīga and Zemgale statistical regions, but in 2018 they were recorded only in Rīga and Kurzeme statistical regions. The mean retail price for 1 kg of king boletes and other kindred mushroom species varied from 7.00 EUR kg–1 (in Zemgale statistical region) to 12.75 EUR kg–1 (in Pierīga statistical region) in 2017 but from 9.25 EUR kg–1 (in Kurzeme statistical region) to 13.50 EUR kg–1 (in Rīga statistical region) in 2018. No statistically significant differences in the mean price were detected between Rīga and Pierīga statistical regions in 2017 (p > 0.05, mean price 11.41 EUR kg–1) or between Kurzeme and Rīga statistical regions in 2018 (p > 0.05, mean price 12.44 EUR kg–1).

Stinkhorn is often used as a natural remedy in folk medicine, and, in 2017 and 2018, there were in total 24 cases in which this mushroom was offered for sale through advertising services or social media, while no sales in markets were recorded. The mean price of stinkhorn was 7.20 EUR kg–1 in 2017 but 15.00 EUR kg–1 in 2018. Most sales took place in Kurzeme statistical region (48% of all cases).

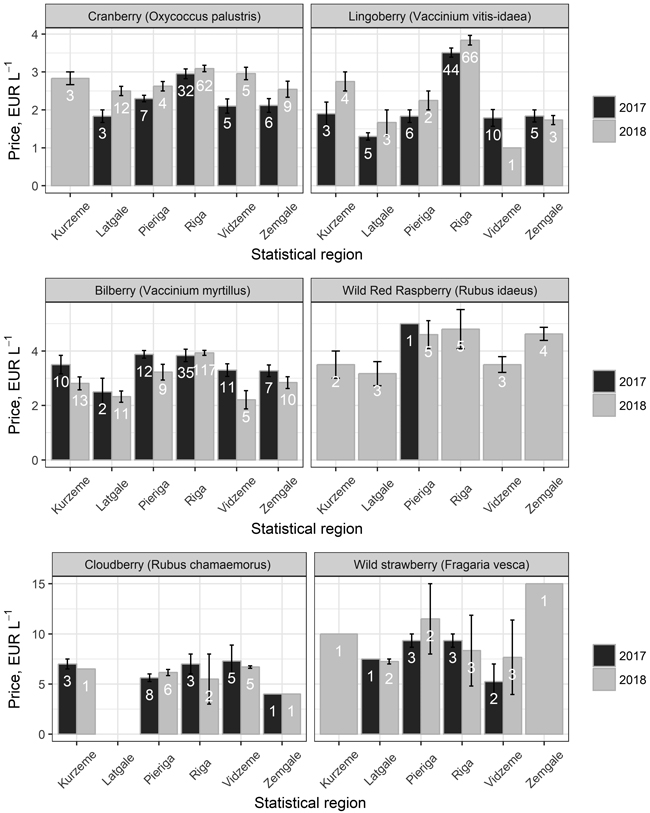

Forest berries account for most of the recorded cases of NWFP sales, and these can be arranged as follows (from the largest to the smallest number of sales): bilberries > lingonberries > cranberries > cloudberries > wild strawberries > wild raspberries. Fig. 4 presents the mean retail prices of the most commonly sold forest berries in Latvia by the statistical regions.

Fig. 4. Mean retail price of wild forest berries in the 2017 and 2018 season by statistical region. White figures in the bars indicate number of cases included in the calculation of mean price.

In 2017, the mean price for 1 L of bilberries varied from 2.50 EUR L–1 (in Latgale statistical region) to 3.88 EUR L–1 (in Pierīga statistical region). In Rīga and Pierīga, the mean retail price for 1 L of bilberries was significantly (on average by 0.53 EUR L–1) higher than that in other statistical regions (p = 0.016). In 2018, the mean price for 1 L of bilberries varied from 2.21 EUR L–1 (Vidzeme statistical region) to 3.93 EUR L–1 (Rīga statistical region). In Rīga, the mean retail price for 1 L of bilberries was significantly (on average by 1.19 EUR L–1) higher than that in other statistical regions (p < 0.001).

In 2017, the mean price for 1 L of lingonberries varied from 1.30 EUR L–1 (in Latgale statistical region) to 3.51 EUR L–1 (in Rīga statistical region). In 2018, the mean price for 1 L of lingonberries varied from 1.00 EUR L–1 (in Vidzeme statistical region) to 3.83 EUR L–1 (in Rīga statistical region). The mean retail price in Rīga statistical region was significantly higher (on average by 1.81 EUR L–1) than that in other statistical regions (p < 0.001).

In 2017, the mean price for 1 L of cranberries varied from 1.83 EUR L–1 (in Latgale statistical region) to 2.95 EUR L–1 (in Rīga statistical region), but, in 2018, the mean price for 1 L of cranberries varied from 2.50 EUR L–1 (in Latgale statistical region) to 3.09 EUR L–1 (in Rīga statistical region). Similar to bilberries and lingonberries, the mean price in Rīga statistical region was significantly higher (on average by 0.84 EUR L–1 in 2017 and by 0.47 EUR L–1 in 2018) than that in other statistical regions (p < 0.001).

The mean price for 1 L of cloudberries in 2017 and 2018 varied from 4.00 EUR L–1 (Zemgale statistical region in 2017 and 2018) to 7.30 EUR L–1 (Vidzeme statistical region in 2017). The number of recorded sales of wild strawberries and wild raspberries was comparatively low – only 6.7% of all cases of forest berry sales. In 2017 and 2018, the mean price for 1 L of wild strawberries varied from 5.25 EUR L–1 to 15.00 EUR L–1, but the mean price for 1 L of wild raspberries varied from 3.17 EUR L–1 to 5.00 EUR L–1.

Table 4 summarizes the changes in the average price of NWFPs and the offered amount in 2018 compared with 2017 (expressed as the number of sales). Although a common trend was not found, the changes in the average retail price for several NWFPs (stinkhorn, Boletes species, birch sap, bilberries and wild raspberries) can be explained by changes in the offered amount of specific products.

| Table 4. Changes in average price of non-wood forest products and offered amount (expressed as number of sales) in 2018 if compared to 2017 in Latvia. | ||

| Non-wood forest products | Change in average price, % | Change in offered amount, % |

| Birch sap | +22.2 | –21.5 |

| Maple sap | +2.6 | +52.4 |

| Chanterelles | –19.1 | –76.6 |

| Boletes species | +10.6 | –71.4 |

| Stinkhorn | +108.3 | –85.0 |

| Bilberry | –1.6 | +144.3 |

| Lingonberry | +26.4 | +8.2 |

| Cranberry | +11.5 | +79.2 |

| Cloudberry | –3.9 | –25.0 |

| Wild strawberry | +12.0 | +33.3 |

| Wild raspberry | –15.9 | +2100* |

| * The extremely large change is explained by very low number of cases in 2017 (n = 1) | ||

Table 5 summarizes the correlation coefficients (r) between the average retail price of NWFPs and the average values of forest characteristics or socio-economic parameters within each statistical region of Latvia in 2017 and 2018 as well as the p-values of the linear model. In the case of socio-economic parameters, the correlation coefficients were > 0.50 in 58% of all the analysed cases, highlighting the significant impact of socio-economic parameters on NWFPs’ retail price in different statistical regions of Latvia. In the case of forest characteristics, a negative correlation between the average price of NWFPs and the forest area or forest cover was predominant, highlighting the impact of the potential availability of NWFPs, which, in turn, affects the offered amount and average retail price of NWFPs. A moderately strong negative correlation (0.52 < r < 0.56) was found between the forest land share of the total land area in a statistical region and the average retail price of birch sap (in 2017 and 2018), wild strawberries (in 2017) and wild raspberries (in 2018). The negative correlation between the forest land share of the total land area in a statistical region and the average retail price of bilberries (in 2018), lingonberries (in 2017) and cranberries (in 2017 and 2018) was even stronger (r > 0.65). At the same time, strong positive correlations (r ranged from 0.69 to 0.97) were found between the estimated potential mean yield of bilberries and lingonberries and the average retail price both in 2017 and in 2018. Although, in many cases, strong correlations were found between the average retail price of NWFPs and the forest characteristics or socio-economic parameters (r > 0.50), these were statistically significant (p < 0.05) only for bilberries, lingonberries and cranberries (grey cells in Table 5).

| Table 5. Correlation coefficients and p-values of linear regression model describing relations between average price of non-wood forest products and forest characteristics or socio-economic parameters in different statistical regions of Latvia in 2017 and 2018 (correlation coefficient r/p-value is shown in table; bold figures indicate r > 0.50 and p < 0.05, grey cells indicate cases when both strong correlation and statistically significant regression was detected). | ||||||||||||

| Parameter | Year | Birch sap* | Maple sap* | Chanter-elles** | Boletes species** | Stink-horn** | Bil-berry* | Lingon-berry* | Cran-berry* | Cloud-berry* | Wild straw-berry* | Wild rasp-berry* |

| Population | 2017 | 0.63/ 0.192 | 0.13/ 0.806 | 0.63/ 0.183 | 0.52/ 0.651 | –0.66/ 0.222 | 0.53/ 0.277 | 0.89/ 0.018 | 0.92/ 0.029 | 0.21/ 0.731 | 0.79/ 0.213 | - |

| 2018 | 0.31/ 0.531 | 0.47/ 0.428 | 0.67/ 0.215 | - | –0.70/ 0.510 | 0.75/ 0.011 | 0.81/ 0.028 | 0.50/ 0.315 | –0.12/ 0.852 | –0.35/ 0.730 | 0.65/ 0.177 | |

| Economically active population (total) | 2017 | 0.59/ 0.225 | 0.13/ 0.805 | 0.64/ 0.175 | 0.53/ 0.645 | –0.65/ 0.234 | 0.57/ 0.242 | 0.90/ 0.014 | 0.93/ 0.021 | 0.22/ 0.725 | 0.78/ 0.222 | - |

| 2018 | 0.27/ 0.580 | 0.51/ 0.377 | 0.69/ 0.197 | - | –0.70/ 0.510 | 0.75/ 0.010 | 0.80/ 0.031 | 0.53/ 0.281 | –0.10/ 0.871 | –0.37/ 0.737 | 0.66/ 0.164 | |

| Economically active population (employed) | 2017 | 0.57/ 0.247 | 0.14/ 0.794 | 0.66/ 0.156 | 0.55/ 0.629 | –0.64/ 0.242 | 0.60/ 0.210 | 0.90/ 0.013 | 0.94/ 0.017 | 0.21/ 0.731 | 0.78/ 0.217 | - |

| 2018 | 0.24/ 0.623 | 0.53/ 0.355 | 0.70/ 0.184 | - | –0.70/ 0.510 | 0.76/ 0.008 | 0.81/ 0.031 | 0.53/ 0.280 | –0.10/ 0.876 | –0.36/ 0.764 | 0.68/ 0.149 | |

| Economically active population (unemployed) | 2017 | 0.75/ 0.076 | <0.01/ 0.993 | 0.24/ 0.642 | 0.25/ 0.841 | –0.63/ 0.252 | 0.06/ 0.912 | 0.72/ 0.109 | 0.66/ 0.226 | 0.27/ 0.666 | 0.56/ 0.445 | - |

| 2018 | 0.73/ 0.101 | 0.11/ 0.864 | 0.35/ 0.561 | - | –0.68/ 0.522 | 0.47/ 0.182 | 0.66/ 0.120 | 0.43/ 0.395 | –0.16/ 0.796 | –0.41/ 0.383 | 0.30/ 0.594 | |

| Economically inactive population | 2017 | 0.72/ 0.113 | 0.13/ 0.810 | 0.59/ 0.215 | 0.50/ 0.668 | –0.70/ 0.192 | 0.43/ 0.399 | 0.84/ 0.036 | 0.85/ 0.066 | 0.20/ 0.748 | 0.80/ 0.197 | - |

| 2018 | 0.43/ 0.385 | 0.31/ 0.615 | 0.60/ 0.290 | - | –0.70/ 0.508 | 0.73/ 0.021 | 0.81/ 0.027 | 0.39/ 0.449 | –0.16/ 0.792 | –0.30/ 0.711 | 0.58/ 0.237 | |

| Unemployment rate | 2017 | 0.17/ 0.683 | –0.31/ 0.555 | –0.78/ 0.065 | –0.96/ 0.188 | 0.13/ 0.835 | –0.98/ <0.001 | –0.49/ 0.323 | –0.64/ 0.244 | 0.09/ 0.891 | –0.49/ 0.506 | - |

| 2018 | 0.65/ 0.188 | –0.74/ 0.157 | –0.71/ 0.183 | - | 0.80/ 0.409 | –0.70/ 0.102 | –0.49/ 0.306 | –0.31/ 0.556 | –0.03/ 0.958 | –0.04/ 0.407 | –0.77/ 0.069 | |

| Number of people with higher education | 2017 | 0.57/ 0.248 | 0.11/ 0.841 | 0.61/ 0.198 | 0.51/ 0.660 | –0.63/ 0.254 | 0.56/ 0.248 | 0.91/ 0.013 | 0.94/ 0.018 | 0.22/ 0.728 | 0.76/ 0.242 | - |

| 2018 | 0.27/ 0.580 | 0.53/ 0.357 | 0.68/ 0.206 | - | –0.68/ 0.524 | 0.74/ 0.012 | 0.79/ 0.037 | 0.55/ 0.260 | –0.11/ 0.864 | –0.38/ 0.722 | 0.66/ 0.164 | |

| Average monthly salaries (Bruto) | 2017 | 0.26/ 0.642 | 0.29/ 0.571 | 0.73/ 0.103 | 0.53/ 0.646 | –0.46/ 0.431 | 0.84/ 0.035 | 0.93/ 0.007 | 0.98/ 0.003 | 0.15/ 0.810 | 0.67/ 0.330 | - |

| 2018 | –0.10/ 0.866 | 0.73/ 0.164 | 0.86/ 0.059 | - | –0.70/ 0.502 | 0.86/ 0.003 | 0.79/ 0.040 | 0.63/ 0.183 | –0.13/ 0.838 | –0.20/ 0.860 | 0.81/ 0.056 | |

| Forest area, kha | 2017 | –0.52/ 0.289 | –0.11/ 0.838 | –0.46/ 0.353 | –0.01/ 0.992 | 0.27/ 0.661 | –0.36/ 0.487 | –0.80/ 0.060 | –0.79/ 0.103 | 0.20/ 0.748 | –0.80/ 0.205 | - |

| 2018 | –0.31/ 0.556 | –0.33/ 0.593 | –0.41/ 0.492 | - | 0.28/ 0.816 | –0.86/ 0.029 | –0.22/ 0.088 | –0.75/ 0.673 | 0.56/ 0.327 | –0.14/ 0.796 | –0.75/ 0.088 | |

| Forest cover, % of total land area | 2017 | –0.56/ 0.250 | –0.04/ 0.935 | –0.18/ 0.728 | 0.17/ 0.892 | 0.29/ 0.636 | –0.09/ 0.861 | –0.68/ 0.092 | –0.74/ 0.203 | 0.08/ 0.897 | –0.56/ 0.438 | - |

| 2018 | –0.55/ 0.261 | –0.16/ 0.798 | –0.24/ 0.701 | - | 0.31/ 0.802 | –0.68/ 0.139 | –0.26/ 0.165 | –0.65/ 0.624 | 0.54/ 0.343 | 0.06/ 0.905 | –0.52/ 0.294 | |

| Potential mean berry yield, kg ha–1 | 2017 | - | - | - | - | - | 0.69 /0.131 | 0.97 /0.001 | *** | *** | *** | *** |

| 2018 | - | - | - | - | - | 0.86 /0.027 | 0.93 /0.008 | *** | *** | *** | *** | |

| Estimated total berry yield, kt | 2017 | - | - | - | - | - | 0.06 /0.906 | –0.53 /0.277 | *** | *** | *** | *** |

| 2018 | - | - | - | - | - | –0.40 /0.427 | –0.27 /0.604 | *** | *** | *** | *** | |

| * Price per 1 L. ** Price per 1 kg. *** No data on potential berry yields available. | ||||||||||||

3.2 Ecosystem service flows of NWFPs

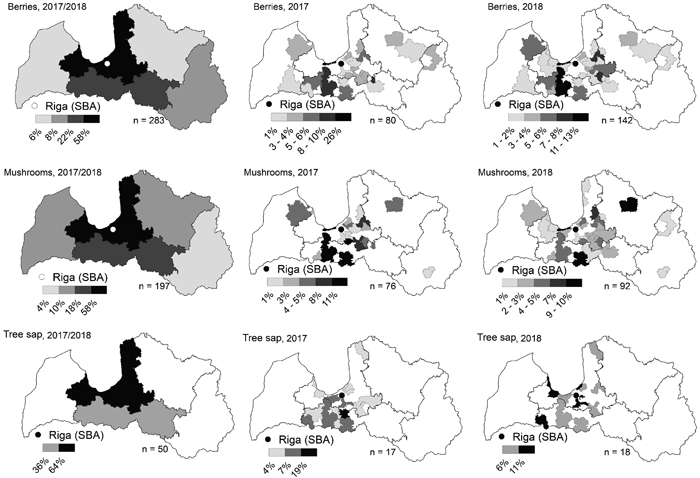

Rīga is the main SBA of the NWFPs in Latvia according to the size of the population (33% of the total population in Latvia). The main SPUs of the NWFP flows to Rīga on the statistical region level are Pierīga and Zemgale (Fig. 5, maps to the left; data for the two seasons are merged, data from the direct interviews). These two are closest to Rīga, and a further breakdown of the SPUs to the county level (Fig. 5, maps in the middle and to the right, separated for 2017 and 2018) demonstrates that, in Pierīga and Zemgale, the number of counties that provide NWFPs to the markets in Rīga is considerably larger than the number in the other statistical regions. Moreover, the counties from which the NWFP flows are recorded are generally rather centrally located – there were few cases or none at all when the NWFPs sold in Rīga’s marketplaces originated from the most peripheral counties of Pierīga and Zemgale statistical regions.

Fig. 5. Main non-wood forest product flows from ecosystem service providing units (statistical regions and counties) to the marketplaces in Rīga in 2017 and 2018. n – number of cases used for flows analysis. Different division in percentages correspond to data structure of every product and year. View larger in new window/tab.

The flow analysis results highlight that flows of berries and mushrooms have larger spatial variety than flows of tree sap, which can most likely be explained by the lower occurrence of sales in general. No SPUs of tree sap to the Rīga marketplaces were recorded in Kurzeme, Vidzeme and Latgale statistical regions. The distance of NWFP flows from SPU to SBA (Rīga) ranges up to approximately 220 km for berries (furthest source providing unit – Balvi county), approximately 241 km for mushrooms (furthest source providing unit – Aglonas county) and approximately 120 km for tree sap.

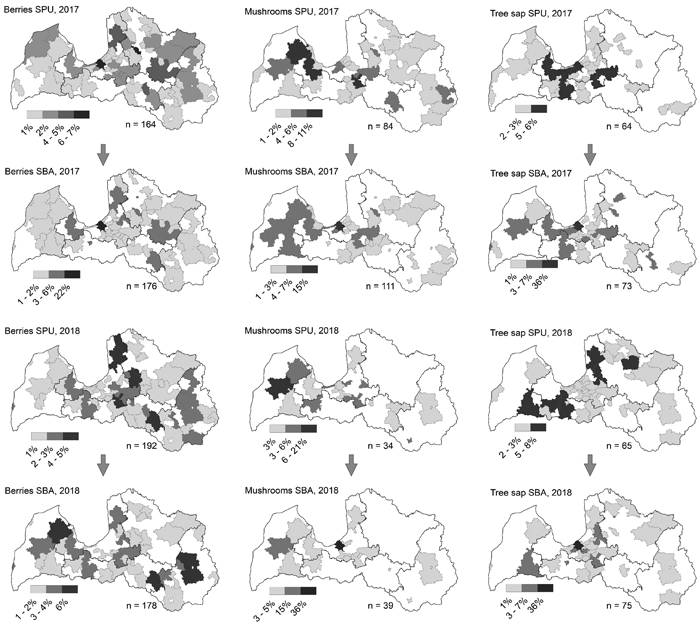

The main non-wood forest product flows from ecosystem service providing units (SPUs) to the service benefitting areas (SBAs), excluding sales in the marketplaces in Rīga, on the county level in 2017 and 2018 are shown in Fig. 6 (data from the telephone interviews). Generally, it appears that there are more SPUs than SBAs and that the number of cases of sales is more evenly distributed in the SBAs than in the SPUs. The coverage of counties both for gathering and for sales of NWFPs is most complete for berries and more complete in 2017 than in 2018. The latter is true for mushrooms as well but not for tree sap. There are several areas where NWFP sales do not occur at all or occur in an extremely small number of cases (e.g., the southwestern part of the country for all products and the entire Vidzeme statistical region for mushrooms in 2018). The geographical pattern of NWFP gathering and sales in the two studied years remained most consistent for berries but least consistent for tree sap.

Fig. 6. Main non-wood forest product flows from ecosystem service providing units (SPU) to the service benefitting area (SBA) excluding sales at marketplaces in Rīga at county level in 2017 and 2018 in Latvia. n – number of cases used for flows analysis. Different division in percentages correspond to data structure of every product and year. View larger in new window/tab.

The average transport distance from tree sap SPUs to SBAs in 2017 was 46 km (n = 32; 50% of cases), not counting cases with lacking information for distance estimation and cases in which both SPU and SBA locations were the same (overlap) (n = 32). The furthest distance measured from the source of origin to the point of utilization was from ~ 180 km. In 2018, the average distance for the tree sap flow was 59 km (n = 32; 49% of cases); cases with the same source/utilization area – 33 (51%). The furthest recorded flow of tree sap was ~ 200 km.

The average distance from mushroom SPUs to SBAs in 2017 was 59 km (n = 25; 30%), and there were 60 cases with the same source/utilization area (70% of cases). The longest recorded distance was ~ 240 km. In 2018, the average flow distance was 52 km, although the sample count used for the distance estimation was relatively small (n = 9; 27% of cases). The number of matching SPU/SBA areas was 25 (73% of cases), and the longest observed flow distance was ~ 120 km.

The average distance from berry SPUs to SBAs in 2017 was 60 km (n = 65; 39% of cases), and there were 104 cases with the same source/utilization area (61% of cases). The maximum flow distance was ~ 250 km. In 2018, the mean distance was estimated at 69 km (from n = 58 or 33% of cases). In 2018, the number of cases in which SPUs and SBAs had the same matching known municipality was 118 (67% of cases). The maximum observed flow distance was ~ 240 km.

The characteristics of the distances to transport non-wood forest products from the SBU to the SBA, including marketplaces in Rīga, are summarized in Table 6. The results reveal that, regardless of whether the SBA is the capital or any other county, the mean value of the transportation distance is similar.

| Table 6. Characteristics of distances to transport non-wood forest product from service providing units (SBU) to service benefitting area (SBA) in 2017 and 2018 in Latvia. | ||||||

| Flow of NWFPs | Cases when NWFPs were transported outside SPU county borders (number/ share)* | Characteristics of distance, km | ||||

| Average value (± S.E.) | Minimum value | Maximum value | Median | Mode | ||

| From SPU to the marketplaces in Rīga | 440/ 100% | 63.1 (1.8) | 14 | 261 | 52.5 | 37 |

| From SPU to SBA in cases when NWFPs were transported outside SPU county borders* | 221/ 37% | 59.7 (3.4) | 6 | 250 | 41 | 30 |

| * SPU and SBA does not match. NWFPs – non-wood forest products. SPU – service providing units. SBA – service benefitting area. | ||||||

4 Discussion

NWFPs are usually gathered within two types of activity. The first one is predominantly recreational when a person, for example, goes to the forest for a walk and additionally harvests some products to take home. Such products are usually self-consumed and can be quantified only with the help of large-scale questionnaires. The second one is the economic activity of harvesting NWFPs with the explicit aim of selling them; the amount of these products, as well as their prices, may be quantified with different methods of market surveys. The largest part of the NWFPs gathered with an economic purpose is sold in the wholesale market. In Latvia, this is an important form of seasonal entrepreneurship in the rural areas and an important economic addition to household budgets, but, at the same time, the wholesale trade of NWFPs has a considerable share of “grey supply chains”, utilizing gaps in the legislation. Interesting research on the bilberry trade chains has been carried out by Mikelis Grivins (see, e.g., Grivins 2016; Grivins et al. 2016; Grivins and Tisenkopfs 2018), but the wholesale trade of NWFPs is beyond the scope of our study. For us, it was interesting to explore the retail market of NWFPs and small-scale seasonal activities of wild product gathering that reflects lifestyle-driven aspects wild product consumption and may provide additional income for families as well.

Among all the analysed non-wood forest product groups, a higher price for a unit was recorded for mushroom species, the highest for stinkhorn and next for Boletes. Among berries, wild strawberries and cloudberries were the most expensive. The price differences between different types of NWFPs is explained by the occurrence of the particular product (bilberries and lingonberries occurring considerably more often and having comparatively much higher yields than other berry species) and the time consumption required for the gathering of a specific product (e.g., based on the opinions expressed by our respondents, cranberry picking is considered less time consuming than, for example, wild strawberry picking).

Within the study, it was detected that NWFPs’ retail price (except stinkhorn) was mostly dependent on population size in the corresponding statistical region of Latvia, that is directly related to the demand for NWFPs. Similarly, positive correlation was detected between NWFPs retail price and number of people with higher education and average monthly salaries in corresponding statistical region that is directly related to the purchasing power. The exception is stinkhorn showing a negative correlation both with population and number of people with higher education. It is related to the long traditions in rural areas where the density of population is significantly smaller, to use stinkhorn for medical purposes (Broks 2003; Dāniele and Meiere 2020). Controversial trends found within the study showing average retail price of NWFPs dependence on multi factorial effects. While negative correlation of the average price of NWFPs with forest cover clearly indicate the logical connection between lower supply and higher demand, it is more complicated to explain positive correlation between potential berry yield and average price of the corresponding berry species. Based on the available data on forest characteristics, we may probably assume that, even with comparatively low forest cover, the yield of bilberry and lingonberry from area unit may still be high, due to suitable forest types and forest structure (this type of analysis was performed only for those two berry species, due to data availability). This seems to be the case for Rīga statistical region where the forest cover is very small but bilberry and lingonberry yield from area unit – high. In our case we had only statistics on total forest cover available, without more specific stand descriptions on the scale of statistical region. Previously conducted research confirms significant differences in berry yields in different forest types and also in forest stands of different density (Donis and Straupe 2011). However, these assumptions should be treated with extreme caution, as the positive correlation may be a result of several different factors and correlation does not necessarily mean causal relationship, particularly in this case, as other factors most likely prevail in determining higher prices for the NWFPs in Rīga.

According to the information provided by the Central Statistical Bureau of Latvia, consumer prices increased by 4.6% during the period from January 2017 to December 2018, but food price changes in 2018 over the corresponding period of previous year ranged from –0.8% (July 2018) to 2.2% (January 2018); average food price change in 2018 over the previous year was 0.7%. Despite the increase of consumer prices, food prices in Latvia were still by 8.2% lower than the EU average (Eurostat 2017). Changes of average retail price of NWFPs in 2018 if compared to 2017 varied in a wide range depending on the type of NWFP. A decrease in the average retail price in 2018 compared with 2017 was observed for chanterelles (–19.1%), wild raspberries (–15.9%), cloudberries (–3.9%) and bilberries (–1.6%). The biggest increase in the average retail price was observed for stinkhorn (+108.3%), lingonberries (+26.4%) and birch sap (+22.2%). The increase in the average retail price of several NWFPs (stinkhorn, lingonberries, birch sap, wild strawberries, cranberries and Boletus species) significantly exceeded the average increase in food prices in Latvia in 2018 compared with 2017. Even though meteorological parameters were not included in the analysis of the given data set, the weather conditions in 2018 were highly unfavourable for several species of berries and mushrooms due to prolonged periods of summer draught. The analysed data set also indirectly characterizes the offered amount of NWFPs. For instance, in 2018, the amount of sales of mushrooms decreased by 78% compared with 2017, and this can be explained by the unfavourable weather conditions in 2018. Generally, the price differences between the years tended to be larger for mushrooms than for berries.

The high impact of the meteorological conditions on the yields of NWFPs (especially of mushrooms, which are more expensive than berries) renders the retail trade of wild products highly unpredictable. Maso (2008) lists high dependence on meteorology and climate and high variability of production amount and quality as the main threats to the commercialization of NWFPs. Under unfavourable circumstances, the number of sales and the turnover in the retail sector decrease sharply. However, on the level of individual cases, the outcome may be quite different. Under unfavourable conditions, the prices are higher, and thus those people who “know the right places” and/or have more time to explore the best locations may benefit to some extent even in “bad years”.

The analysis of the flows of NWFPs revealed that at least in half of all cases the products were utilized in the same area as they were gathered. The utilization in situ was highest for mushrooms (approximately 70% of all cases) and lowest for tree sap, where in situ utilization and directional flows made up a similar number of cases.

In Latvia, the forest berries, mushrooms and tree sap that are offered in retail trade should be considered as exclusive products rather than as simple additions to everyday diet. The use of the NWFPs is largely related to lifestyle, the near-to-nature philosophy and the slow-food movement, especially in the capital city, Rīga. The observations of the research team in the marketplaces and the interviews with the retailers gave evidence that the number of customers is sufficient and there is a stable demand for NWFPs. Rīga is the major market for NWFPs, as, in rural areas, the level of income is lower and a larger amount of people gather the NWFPs themselves. Thus, it may be assumed that the purchasing capacity of the customers, at least in Rīga, is sufficient, as confirmed by the higher prices of NWFPs in Rīga than in the other SBAs. The prices were considerably higher at the start and the end of the season. Since this study covers only Rīga’s markets and sampled retailers in other parts of Latvia (mostly small businesses or individuals), there is still a considerable question concerning aspects of industrialized use of some of the NWFPs, for example those used in other products or sold in large batches used for exporting (frozen berries, pulp, juices and others).

Existing studies on the NWFP market in the EU have shown that the available information is highly variable, incomplete and incomparable among the member states (Turtiainen and Nuutinen 2012). At the same time, there is a growing interest among forest owners in the potential financial gains of NWFP sales, while implementing multi-objective forest management and considering that not only meteorological conditions but also forest management decisions have an impact on the occurrence and yield of forest berries and mushrooms (Miina and Kurttila 2017). Forest planning and management activities can affect the provision of NWFPs , and the ecosystem service approach offers possibilities to involve multiple stakeholders and perform more complex NWFP assessments (Huber et al. 2019). It is important to advance studies on the impact of forest management on NWFP yields, including spatial and temporal modelling approaches to enable more accurate forest management.

Our study results display tangible evidence of spatial mismatches between the provision of ecosystem services and the actual beneficiary locations of these services. The maps clearly identify the broad range of supply for these non-wood forest products. Further studies can assess such spatial dispersions from the perspective of forest planning. Considering the double importance of the NWFPs as provisioning and cultural ecosystem service, more accurate information on the spatial distribution of their flows may contribute to the implementation of multi-purpose forest management. For example, in areas that are highly suitable for NWFP gathering (both from the perspective of potential yields and accessibility), the aims of forest management might be adjusted accordingly. The approach of expanding forest categories and introducing a new one – forest with important NWFP functions – has been suggested by Sisak et al. (2016) for the Czech Republic. Similarly, the supply–demand balance of NWFPs on the spatial and temporal scales, market saturation, profiles of NWFP users and underlying philosophy of their use are among the topics of interest for further research that would necessarily involve a more interdisciplinary approach than we were able to incorporate into the current study. Studies revealing undisclosed motivations and necessities of salesmen and de facto producers (person or groups gathering the products in forests) should be explored, and further opinions from forest owners and managers could complement such information to build a broad, insightful and inclusive view of future developments in NWFP use.

5 Conclusions

1. Monitoring of retail market offered a useful dataset for analysis of NWFP prices and flows.

2. The average prices of specific NWFPs reflect their availability, as well as time consumption needed for their gathering. Generally, the retail prices of NWFPs varied considerably between the years; it is most likely that the variation was due to the wild product yields, influenced mainly by the meteorological conditions.

3. The geographical distribution of NWFP service providing units and service benefitting areas varied considerably between the years.

4. The retail trade of NWFPs may provide additional income for households, but this source of income is unstable due to the varying conditions. The yield of the most expensive NWFPs, mushrooms, was highly variable both on a spatial basis and between consecutive years.

Acknowledgements

The study was implemented with financial and technical support from JSC “Latvia’s State Forests” in the framework of the research programme “The impact of forest management on ecosystem services provided by forests and related ecosystems” (Nr. 5-5.5_006_101_16_6), implemented by LSFRI “Silava”. We thank the anonymous reviewers for their constructive comments.

References

Burkhard B., Kandziora M., Hou Y., Müller F. (2014). Ecosystem service potentials, flows and demands – concepts for spatial localisation, indication and quantification. Ladscape Online 34: 1–32. https://doi.org/10.3097/LO.201434.

Broks J. (2003). Meža enciklopēdija. [Forest encyclopedia]. Apgāds Zelta Grauds, Rīga. 368 p. [In Latvian].

Cabinet Order No 271 (2004). On statistical regions of the Republic of Latvia and administrative units therein. https://likumi.lv/ta/en/en/id/88074. [Cited 16 Jan 2020].

Calama R., Tomé M., Sánchez-González M., Miina J., Spanos K., Palahí M. (2010). Modelling non-wood forest products in Europe: a review. Forest Systems 19: 69–85. https://doi.org/10.5424/fs/201019S-9324.

Central Statistical Bureau of Latvia (2019). https://www.csb.gov.lv/en/sakums. [Cited 16 Jan 2020].

Cesaro L., Linddal M., Pettenella D. (1995). The economic role of non-wood forest products and services in rural development. Medit 6(2): 28–34.

Common International Classification of Ecosystem Services (2013). http://www.cices.eu. [Cited 16 Jan 2020].

Dāniele I., Meiere D. (2020). Lielā Latvijas sēņu grāmata. [The big book of Latvian mushrooms]. Latvijas Dabas muzejs, Karšu izdevniecība Jāņa seta, Rīga. 528 p. [In Latvian].

Donis J. (2018). Rekreācijas preferences dažādos gadalaikos. [Recreational preferences in different seasons]. Report on research programme “The impact of forest management on ecosystem services provided by forests and related ecosystems” results in 2017. p. 245–265.

Donis J., Straupe I. (2011). The assessment of contribution of forest plant non-wood products in Latvia’s national economy. Research for Rural Development Annual 17th International Scientific Conference Proceedings 2: 59–64.

Eurostat (2017). Consumer price levels in the EU. https://ec.europa.eu/eurostat/news/themes-in-the-spotlight/price-levels-2017. [Cited 16 Jan 2020].

FAO (2010). Global forest resources assessment 2010. http://www.fao.org/3/a-i1757e.pdf. [Cited 16 Jan 2020].

FAO (2015). Terms and definitions. Forest Resource Assessment Working paper 180. http://www.fao.org/docrep/017/ap862e/ap862e00.pdf. [Cited 16 Jan 2020].

Grivins M. (2016). A comparative study of the legal and grey wild product supply chains. Journal of Rural Studies 45: 66–75. https://doi.org/10.1016/j.jrurstud.2016.02.013.

Grivins M., Tisenkopfs T. (2018). Benefitting from the global, protecting the local: the nested markets of wild product trade. Journal of Rural Studies 61: 335–342. https://doi.org/10.1016/j.jrurstud.2018.01.005.

Grivins M., Tisenkopfs T., Stojanovic Z., Ristic B. (2016). A comparative analysis of the social performance of global and local berry supply chains. Sustainability 8(6) article 532. https://doi.org/10.3390/su8060532.

Grīviņš M. (2015). Forests made of money: multidimensional properties of the wild blueberry sector’s development. Proceedings of the University of Latvia 808: 52–76. [In Latvian].

Hamunen K., Kurttila M., Miina J., Peltola R., Tikkanen J. (2019). Sustainability of Nordic non-timber forest product-related businesses – a case study on bilberry. Forest Policy and Economics 109 article 102002. https://doi.org/10.1016/j.forpol.2019.102002.

Huber P., Hujala T., Kurttila M., Wolfslehner B., Vacik H. (2019). Application of multi criteria analysis methods for a participatory assessment of non-wood forest products in two European case studies. Forest Policy and Economics 103: 103–111. https://doi.org/10.1016/j.forpol.2017.07.003.

Jeanrenaud S. (2008). Communities and forest management in western Europe. IUCN, Working Group on Community Involvement in Forest Management. 170 p.

Kangas J., Niemeläinen P. (1996). Opinion of forest owners and the public on forests and their use in Finland. Scandinavian Journal of Forest Research 11(1–4): 269–280. https://doi.org/10.1080/02827589609382936.

Keča L.J., Keča N., Rekola M. (2013). Value chains of Serbian non-wood forest products. International Forestry Review 15(3): 315–335. https://doi.org/10.1505/146554813807700164.

Kovalčík M. (2014). Value of forest berries and mushrooms picking in Slovakia´s forests. Beskydy 7(1): 39–46. https://doi.org/10.11118/beskyd201407010039.

Kurttila M., Pukkala T., Miina J. (2018). Synergies and trade-offs in the production of NWFPs predicted in boreal forests. Forests 9(7) article 417. https://doi.org/10.3390/f9070417.

Latvijas Republikas Saeima (2000). Law on forests. https://likumi.lv/ta/en/en/id/2825-law-on-forests. [Cited 16 Jan 2020].

Latvian NFI data (2015). Latvian National Forest Inventory database. http://www.silava.lv/petijumi/nacionlais-mea-monitorings.aspx. [Cited 16 Jan 2020].

Lībiete Z. (2017). Aptauja par Latvijas iedzīvotājiem nozīmīgākajiem meža ekosistēmu pakalpojumiem. [Most important forest ecosystem services in the view of inhabitants of Latvia]. Report on research programme “The impact of forest management on ecosystem services provided by forests and related ecosystems” results in 2016. p. 76–84. [In Latvian].

Lõhmus A., Remm L. (2017). Disentangling the effects of seminatural forestry on an ecosystem good: bilberry (Vaccinium myrtillus) in Estonia. Forest Ecology and Management 404: 75–83. https://doi.org/10.1016/j.foreco.2017.08.035.

Martinez de Aragon J.M., Riera P., Giergiczny M., Colinas C. (2011). Value of wild mushroom picking as an environmental service. Forest policy and Economics 13(6): 419–424. https://doi.org/10.1016/j.forpol.2011.05.003.

Maso D. (2008). Networks and PES schemes as income-generation tools for the development of the Italian forest sector. PhD thesis. University of Padova. 110 p.

Miina J., Kurttila M. (2017). Multiproduct forest management planning – the case of timber and bilberry production. http://www.fao.org/forestry/nwfp/93068/en/. [Cited 16 Jan 2020].

Neumann R.P., Hirsch E. (2000). Commercialization of non-timber forest products: review and analysis of research. CIFOR, Dzakharta. 176 p.

Parviainen J. (2015). Cultural heritage and biodiversity in the present forest management of the boreal zone in Scandinavia. Journal of Forest Research 20(5): 445–452. https://doi.org/10.1007/s10310-015-0499-9.

Pouta E., Sievänen T., Neuvonen M. (2006). Recreational wild berry picking in Finland – reflection of a rural lifestyle. Society and Natural Resources 19(4): 285–304. https://doi.org/10.1080/08941920500519156.

Rowland D., Ickowitz A., Powell B., Nasi R., Sunderland T.C.H. (2016). Forest foods and healthy diets: quantifying the contributions. Environmental Conservation 44(2): 102–114. https://doi.org/10.1017/S0376892916000151.

Saastamoinen O., Matero J., Horne P., Kniivilä M., Haltia E., Mannerkoski H., Vaara M. (2014). Classification of boreal forest ecosystem goods and services in Finland. Reports and studies in forestry and natural sciences, University of Eastern Finland. 197 p.

Shackleton S., Gumbo D. (2010). Contribution of non-wood forest products to livelihoods and poverty alleviation. In: Chidumayo E.N, Gumbo D.J. (eds.). The dry forests and woodlands of Africa. Managing for products and services. p. 63–91. https://doi.org/10.4324/9781849776547.

Schulp C.J.E., Thuiller W., Verburg P.H. (2014). Wild food in Europe: a synthesis of knowledge and data of terrestrial wild food as an ecosystem service. Ecological Economics 105: 292–305. https://doi.org/10.1016/j.ecolecon.2014.06.018.

Sisak L., Riedl M., Dudik R. (2016). Non-market non-timber forest products in the Czech Republic – their socio-economic effects and trends in forest land use. Land Use Policy 50: 390–398. https://doi.org/10.1016/j.landusepol.2015.10.006.

Stanley D., Voeks R., Short L. (2012). Is non-timber forest product harvest sustainable in the less developed world? A systematic review of the recent economic and ecological literature. Ethnobiology and Conservation 1(9): 1–39. https://doi.org/10.15451/ec2012-8-1.9-1-39.

Stryamets N., Elbakidze M., Ceuterick M., Angelstam P., Axelsson R. (2015). From economic survival to recreation: contemporary uses of wild food and medicine in rural Sweden, Ukraine and NW Russia. Journal of Ethnobiology and Ethnomedicine 11 article 53. https://doi.org/10.1186/s13002-015-0036-0.

Stryamets N., Elbakidze M., Chamberlain J., Angelstam P. (2020). Governance of non-wood forest products in Russia and Ukraine: institutional rules, stakeholder arrangements, and decision-making processes. Land Use Policy 94 article 104289. https://doi.org/10.1016/j.landusepol.2019.104289.

Tahvanainen V., Kurttila M., Miina J., Salo K. (2016). Non-wood forest products boosting the North Carelian bioeconomy. Natural Resources Institute Finland. 12 p.

The Supreme Council of the Republic of Latvia (1993). Law on personal income tax. https://likumi.lv/ta/en/en/id/56880-on-personal-income-tax. [Cited 16 Jan 2020].

Turtiainen M., Nuutinen T. (2012). Evaluation of information on wild berry and mushroom markets in European countries. Small-scale Forestry 11: 131–145. https://doi.org/10.1007/s11842-011-9173-z.

Weiss G., Emery M.R., Corradini G., Živojinović I. (2020). New values of non-wood forest products. Forests 11(2) article 165. https://doi.org/10.3390/f11020165.

Wiersum K.F. (2017). New interest in wild forest products in Europe as an expression of biocultural dynamics. Human Ecology 45: 787–794. https://doi.org/10.1007/s10745-017-9949-7.

Total of 47 references.